174 Days. 8 Days. Fully Recovered.

A small-ticket fintech lender. A borrower 174 days past due after seven months of traditional collections had already failed. Eight days from allocation to Collekt to full recovery.

Impact at a Glance

| 7 mo | Prior failed collections |

| 174 | Days past due at allocation |

| 8 | Days from allocation to full recovery |

| 100% | Recovered — ₹2,093 in full |

Seven months of traditional collections. Then us.

At 174 days past due on a ₹2,093 loan, this borrower had already been through the standard playbook. Seven months of high-intensity, low-intelligence activity: relentless outbound calls, SMS campaigns on a vertical channel basis, each channel firing independently with no shared intelligence and no sense of who the borrower actually was.

It hadn't worked. Not because she couldn't pay. Because nobody had listened.

At this stage, lenders have made their decision and handed to agencies. Agencies work no-win no-fee. That model is not structured to solve the borrower's problem — only to collect or move on. There are no other platforms operating here. Collekt was allocated on 2nd June 2026. Before sending a single message, the system read the signals.

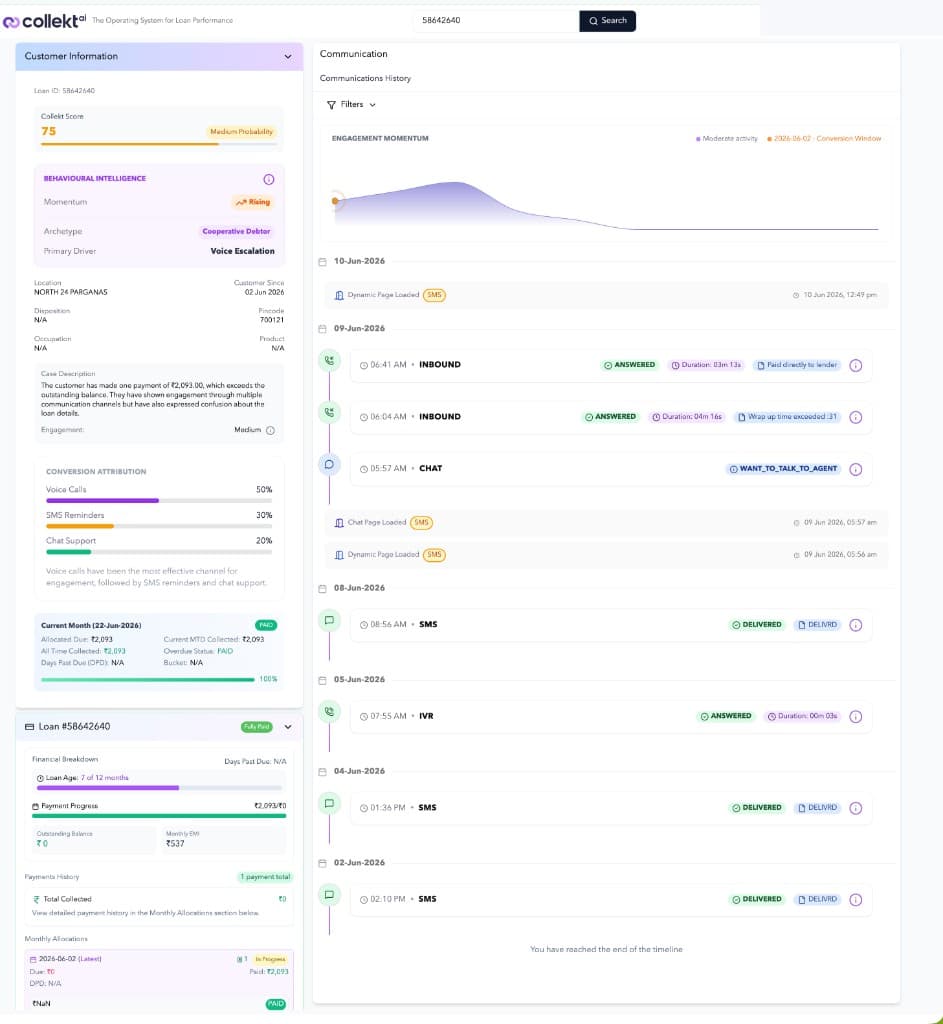

Case at Allocation

| Days Past Due | 174 DPD |

| Overdue Amount | ₹2,093 |

| Lender Type | Small-ticket fintech |

| Prior Collections | 7 months. High intensity, low intelligence. Agency involved. |

| Prior Approach | Relentless outbound. Vertical channels. No resolution. |

What Collekt Read

| Collekt Score | 75 — Medium Probability |

| Behavioural Archetype | Cooperative Debtor |

| Engagement Momentum | Rising |

| Signals Detected | Opened payment page link, listened to IVR, chat tonality, escalation pattern |

| Cascade Decision | Digital nudges only. Coaching tone. No pressure. |

Eight days. Every touchpoint earned.

No outbound calls were made. After seven months of being chased relentlessly, the system gave her room. It let her move at her own pace and surfaced the right channel at the right moment.

02 Jun 2026 — Allocation · System

Cooperative archetype identified. SMS-only cascade assigned.

After seven months of high-intensity traditional collections, Collekt read the signals differently. Score: 75. Momentum rising. Cooperative debtor. The instruction to the cascade: no outbound calls, coaching tone, digital nudges only. Let her come to us.

02 Jun – 08 Jun (IST) · SMS

Three SMS messages delivered. IVR answered briefly on day 3.

Each delivery logged and read by the system. The IVR engagement on 5th June at 1:25 PM IST lasted 3 seconds — enough to confirm the number was live and the borrower was reachable. Momentum noted. The approach held steady.

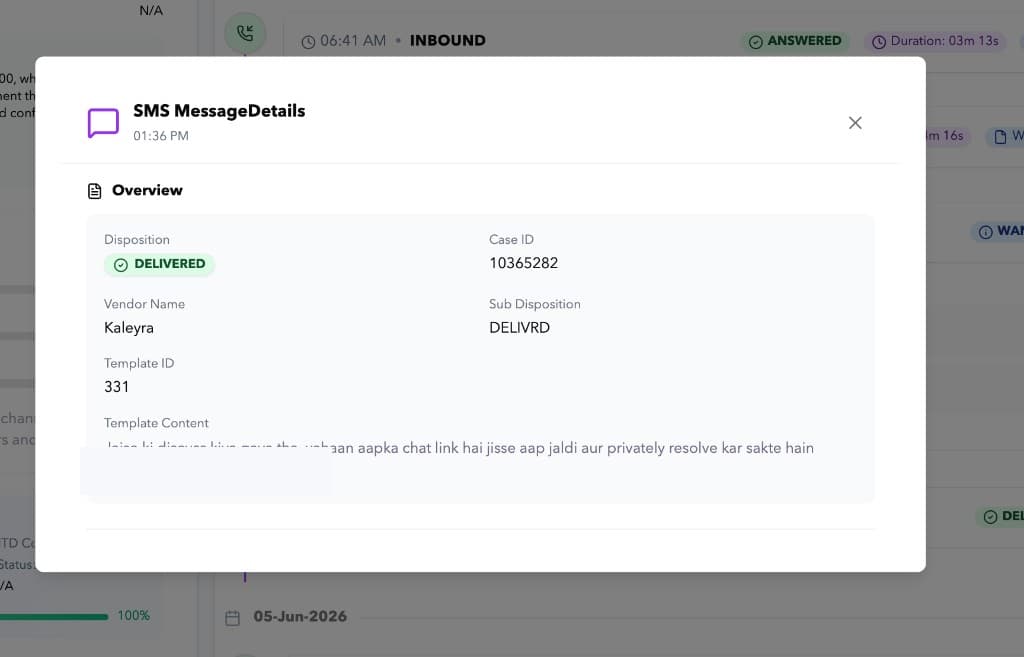

SMS — chat link for private resolution

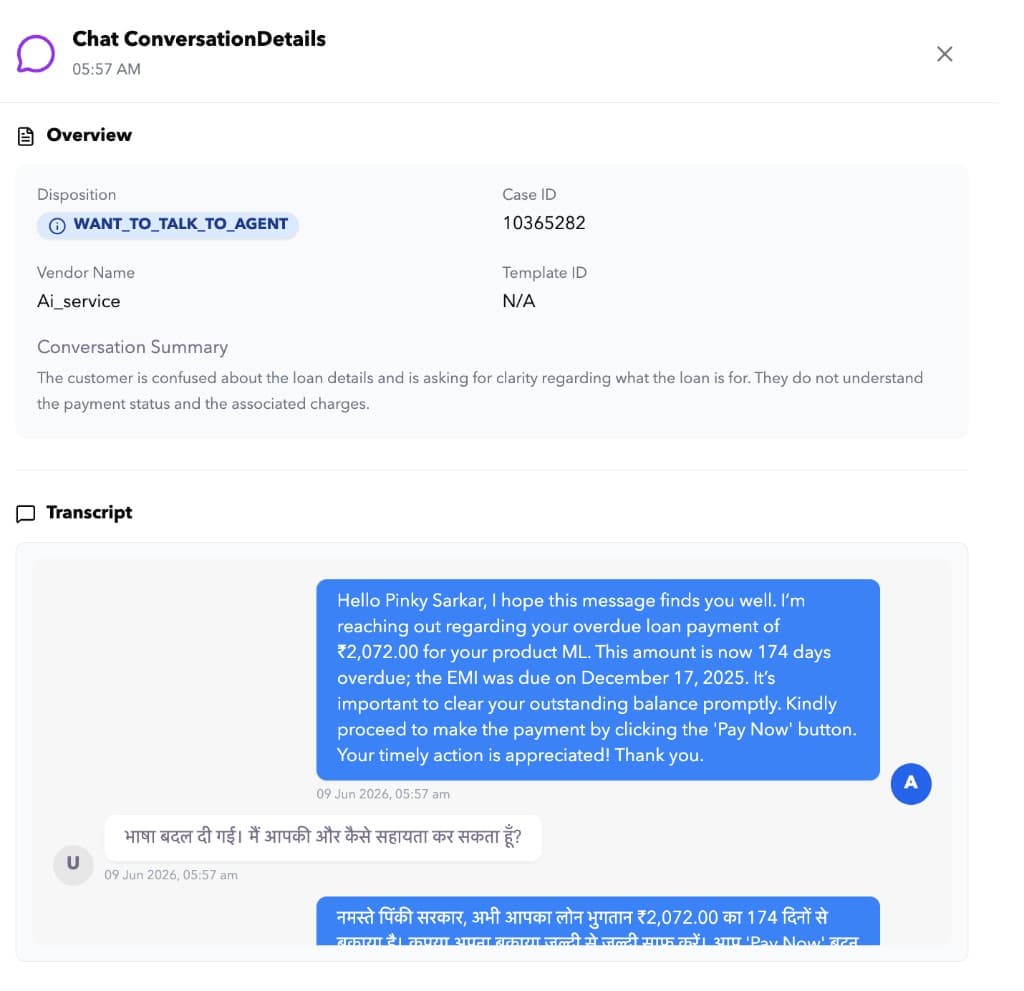

09 Jun, 11:27 AM IST · Chat

Borrower opens SMS link. Enters chat. Asks about the loan.

The chat was handled by Collekt's proprietary Small Language Model — trained as a collections expert on over a billion data points. Her opening message arrived in Hinglish. The SLM switched seamlessly to Hindi without a prompt or a pause. Her question was straightforward: what is this loan, I don't understand the charges. The SLM read the tonality, recognised this as a moment requiring human reassurance rather than more automation, and asked directly: would you like me to connect you with an agent? It provided the number. Not a script fallback. A deliberate, trained escalation decision.

Chat conversation — SLM switches Hinglish to Hindi, offers human agent connection

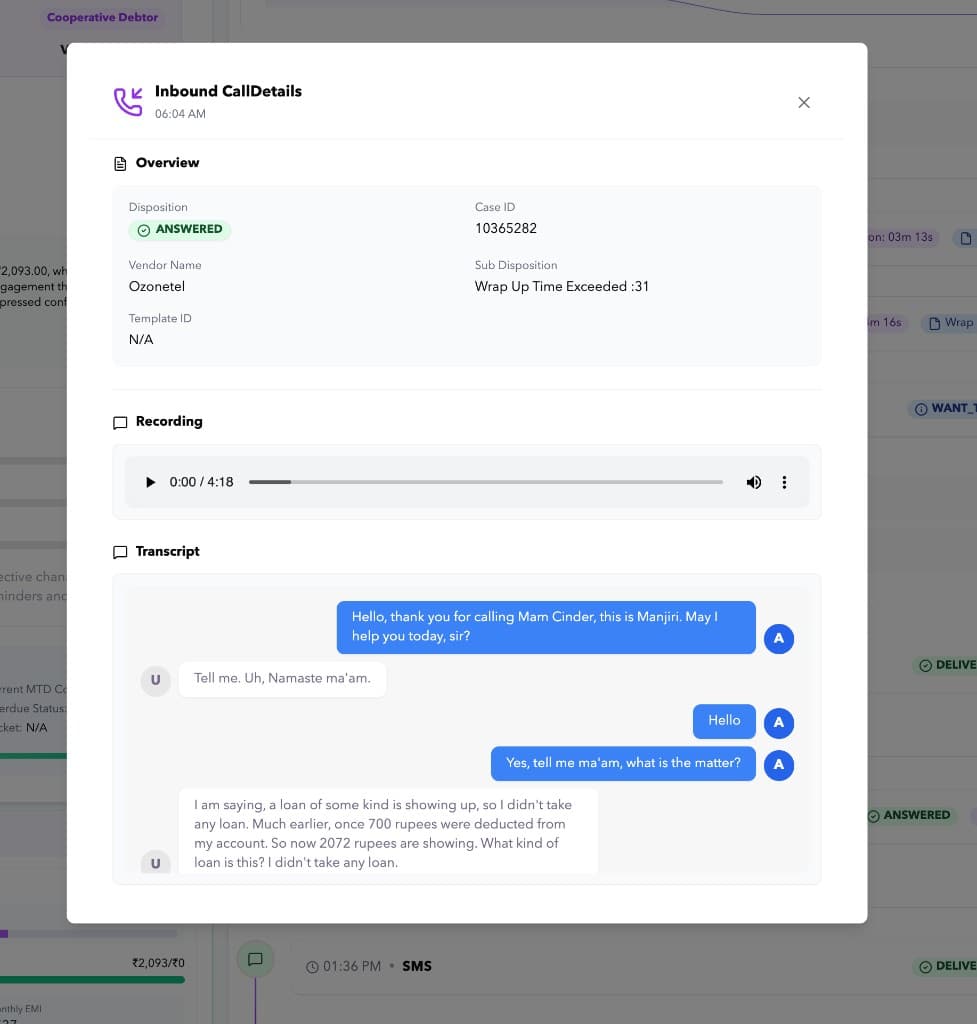

09 Jun, 11:34 AM IST — 4m 16s · Inbound Call

She calls in. Gets clarity — without repeating herself.

Before the call connected, the Collekt platform had already briefed the agent: the chat transcript, the confusion she'd expressed, her payment history, her archetype. She didn't have to explain herself from scratch to someone reading from a script. The agent already knew why she was calling and responded with context. She explained the loan confusion, got a clear answer, and hung up to make the payment herself.

First inbound call, 11:34 AM IST — agent pre-briefed, borrower confusion resolved

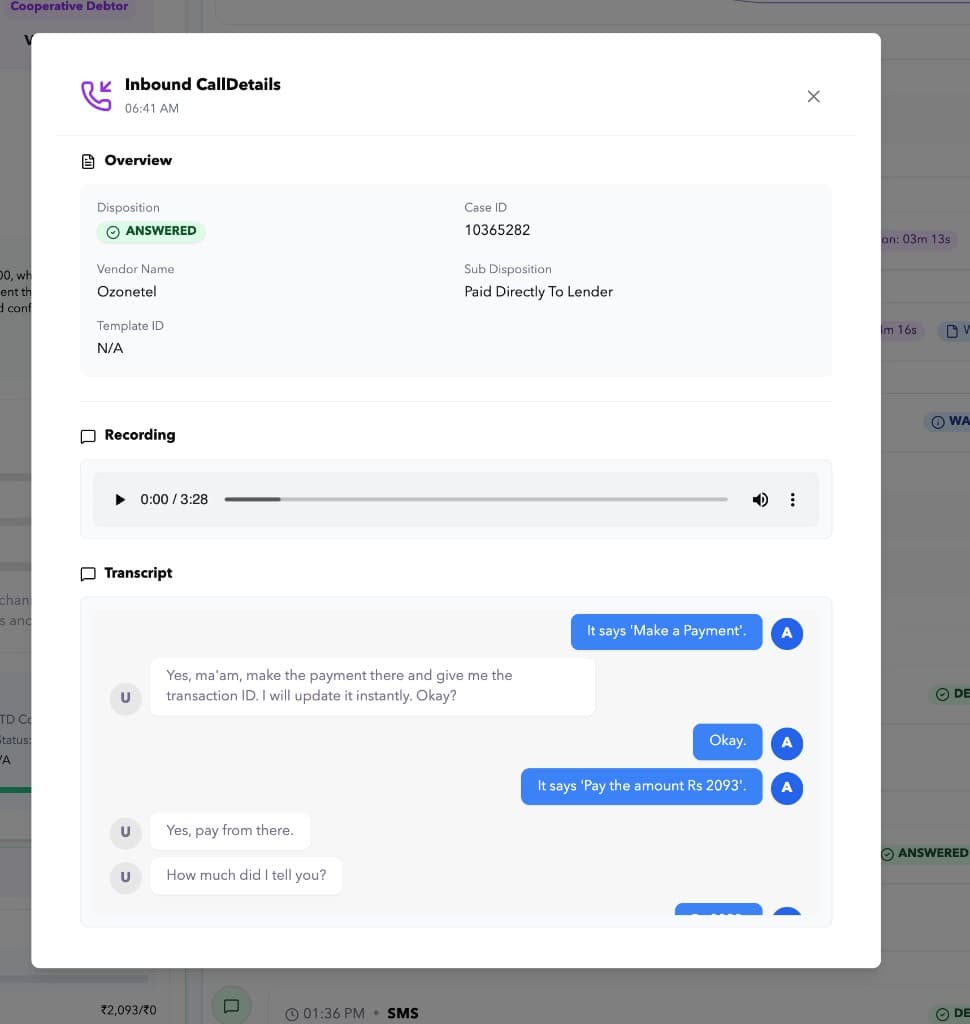

09 Jun, 12:11 PM IST — 3m 13s · Inbound Call

She calls back. Needs help navigating the payment screen.

She found the payment page but needed a hand. The agent walked her through: click Make a Payment, pay ₹2,093, share the transaction ID. She paid during the call. Sub-disposition: Paid Directly to Lender.

Second inbound call, 12:11 PM IST — agent assisted payment. Sub-disposition: Paid Directly to Lender

09 Jun 2026 — Day 8 · Resolved

₹2,093 recovered in full. Case closed.

Loan status: Fully Paid. Overdue status: Paid. Outstanding balance: ₹0.

Full case view — Collekt portal

Seven months of the wrong approach

Traditional collections isn't broken because of bad intentions. It's broken because the model doesn't require understanding. Outbound calls, SMS, agency referral — all firing on vertical channel tracks, relentlessly, until collected or abandoned. No-win no-fee agencies have no structural incentive to understand the borrower. They have an incentive to collect or move to the next case.

After seven months of that, she still hadn't paid. Not because she was a bad borrower. Because she was confused and nobody had offered clarity.

| Traditional Approach | Collekt | |

|---|---|---|

| Prior history | 7 months. Relentless outbound calls, SMS, agency. High intensity, no intelligence. | Allocated after 7 months. Read signals from day one. Different approach entirely. |

| Channel approach | Vertical. Each channel fires independently. No shared intelligence between them. | Orchestrated. Every signal feeds back into the cascade decision in real time. |

| Day 1 action | Outbound dial campaign. Script-driven. Same approach on day 1 as month 7. | SMS nudge only. Cooperative archetype flagged. No pressure applied. |

| Agency incentive | No-win no-fee. Not structured to understand or solve the borrower's problem. | Intelligence-led. Resolution is the outcome, not just collection activity. |

| Language handling | Single-language script. Hinglish or dialect mismatch ends the interaction. | SLM switched seamlessly from Hinglish to Hindi mid-conversation. |

| Escalation to human | No mechanism to detect confusion or route to a human in real time. | SLM identified the moment reassurance was needed and offered the connection directly. |

| Agent briefing | Borrower re-explains from scratch to an agent reading a script. | Agent briefed with full context before the call connected. No repetition. |

| Borrower confusion | Missed entirely. Script continues regardless. | Captured in chat as WANT_TO_TALK_TO_AGENT. Escalated to human in real time. |

| 174 DPD routing | Agency referral. Relationship with lender damaged. | Held in digital + inbound channel. Zero agency involvement. |

| Second inbound call | No mechanism to receive or route it | Agent available. Walked her through payment in 3 minutes. |

| Outcome | Dispute, avoidance, or partial agency recovery | Full recovery. 8 days. Borrower relationship intact. |

Numbers that speak for themselves

We're not sharing this case because it's exceptional. We're sharing it because it isn't. The same intelligence, the same orchestration, the same signal observability runs across every case in a lender's book simultaneously — from micro loans like this one through MFI portfolios, bank unsecured, credit cards, and B2B trade receivables finance. The principle doesn't change with ticket size.

| ₹2,093 | Recovered in full |

| 8 days | From allocation to resolution |

| 0 | Outbound pressure calls |

This case was handled end-to-end by the Collekt agentic platform. The SLM managed the conversation, read the signals, and made the escalation decision. The platform routed the inbound call and briefed the agent. The only moment a human was involved was the one moment a human was needed — when a borrower who had spent seven months being chased by strangers finally needed someone to listen.

That is how Collekt runs over a million cases a month. 96% of them never need a human at all.

| 96% | Of resolutions with zero human involvement |

| 1.4M+ | Cases processed per month |

Seven months of relentless traditional collections produced nothing. Eight days of listening produced full payment. Understanding the borrower isn't a nice-to-have. It's the only thing that works.

Case study — India lending market. All borrower data anonymised.

Frequently asked questions

- What was the borrower situation at allocation?

- The borrower was 174 days past due on a ₹2,093 loan after seven months of high-intensity traditional collections — relentless outbound calls, SMS campaigns, and agency involvement — that had failed to resolve the case. Collekt was allocated on 2 June 2026.

- How did Collekt classify this borrower before any outreach?

- Collekt scored the case at 75 (medium probability), identified a Cooperative Debtor behavioural archetype with rising engagement momentum, detected signals including payment page opens, IVR engagement, chat tonality, and escalation patterns, and assigned a coaching-tone SMS-only cascade with no outbound pressure calls.

- Why did the borrower eventually pay?

- The borrower was confused about the loan and charges, not avoidant. After seven months of being chased relentlessly, Collekt SLM handled the chat in Hinglish and Hindi, offered a direct connection to an agent, and escalated appropriately. She called in twice — first for clarity with a fully briefed agent, then for help navigating the payment screen — and paid ₹2,093 in full during the second call.

- How does this compare to a traditional collections approach?

- Traditional collections ran for seven months with vertical channel firing, script-driven outbound, agency referral, and no shared intelligence. Collekt orchestrated signals in real time, held pressure back, switched language mid-conversation, escalated confusion immediately, and briefed the agent with full context before the call connected.

- What was the final outcome?

- ₹2,093 recovered in full on 9 June 2026 — day 8 from Collekt allocation. Loan status: Fully Paid. Outstanding balance: ₹0. Zero outbound pressure calls made.